The narrative of high-growth technology has been localized to a few zip codes in Northern California for far too long. We have been conditioned to believe that if you want to build a world-changing company, you must be on Sand Hill Road.

That narrative is an outdated movie we’ve all seen before. While the herd remains trapped in the echo chamber of Silicon Valley, the actual center of gravity has already left the building.

Look at the application layer of AI. A recent study of the top 50 consumer AI apps shows that three of the most dominant players are built by a single company, Codeway, based in Turkey. Innovation isn’t just migrating; it has already been exported. The future is being written “Elsewhere.”

The “Great Flip” and the Rise of the Access Class

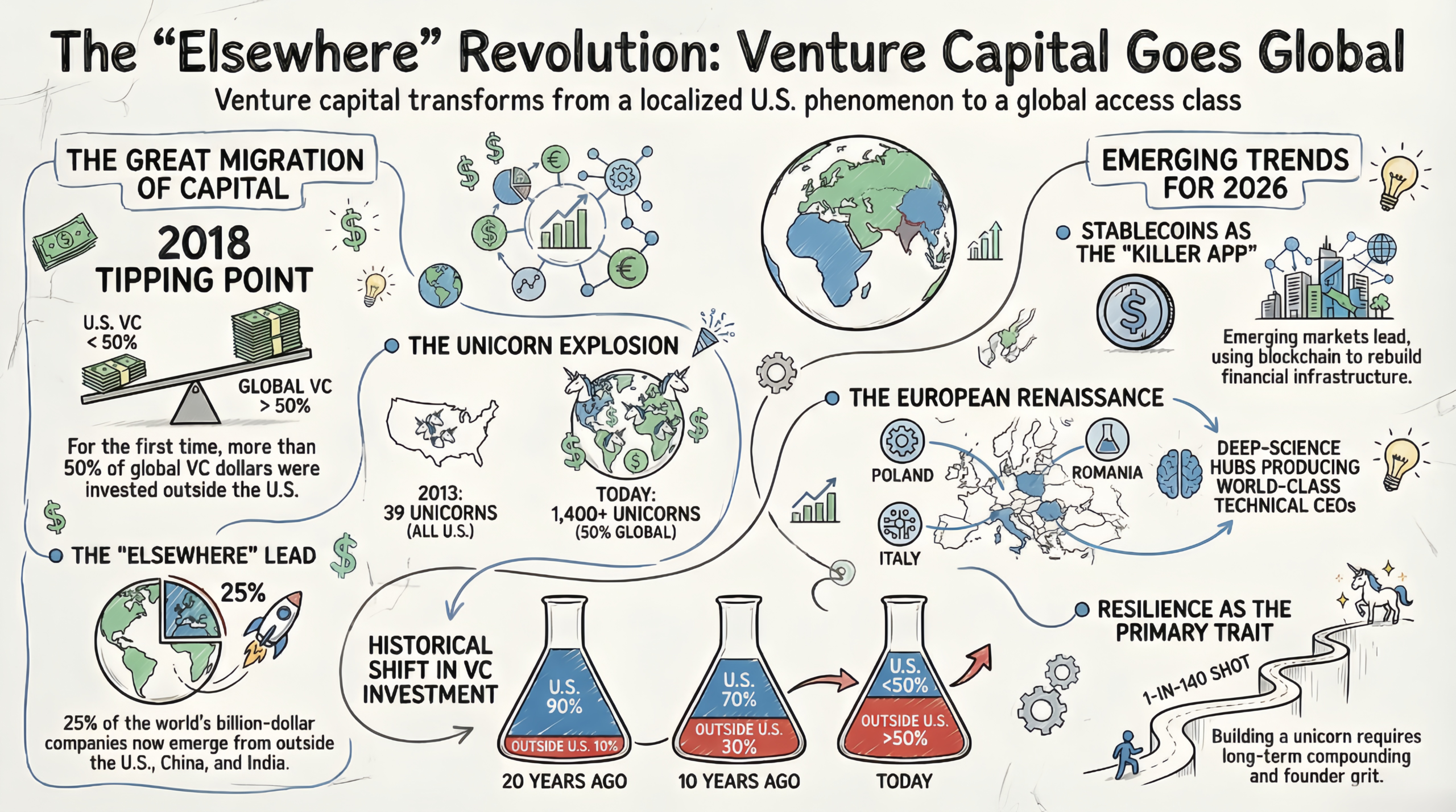

The geographical distribution of venture dollars has undergone a radical transformation. Twenty years ago, 90% of all venture capital was invested in the United States. Today, the world looks completely different.

The tipping point occurred in 2018. For the first time in history, more than 50% of global venture capital was invested outside the U.S. While the “Top 6” markets—China, India, the UK, Germany, Israel, and France—capture 80% of those non-U.S. dollars, the real alpha is found in the frontier.

Venture is no longer just an asset class; it is an “Access Class.” Success depends on who has the boots on the ground in markets like Brazil—which is now Endeavor’s #1 market in the world—Mexico, and Indonesia. These are the hubs where the next $100 billion companies are being forged.

The Statistical Miracle: How “Elsewhere” Captured the Unicorn

In 2013, Aileen Lee coined the term “Unicorn” to describe the statistical anomaly of a $1 billion private company. At that time, there were only 39 in existence, and every single one of them was in the United States.

Today, there are over 1,400 unicorns, and the U.S. share has plummeted to 50%. The rest of the world has caught up, with “Elsewhere”—Southeast Asia, the Middle East, LatAm, and Europe—accounting for a full 25% of the total.

A high-profile Stanford study recently attempted to rank the best unicorn investors but ignored 50% of the world because the data was “too hard to get.” This oversight blinded them to the reality that the odds of building a unicorn are 1 in 140—a 0.7% chance. These statistical miracles are now happening daily in regions that traditional VCs still struggle to find on a map.

The Strategic Edge of Forced Patience: Why Locked Capital Wins the Long Game

In a world of day-trading and instant gratification, the greatest strategic advantage is illiquidity. As Warren Buffett and Charlie Munger famously noted, “the big money is not in the buying or the selling, it’s in the waiting.”

Illiquidity is a feature, not a bug. It acts as a protective shield, preventing investors from selling their stakes due to temporary fear or greed. Because company building is a 10-to-20-year journey, “locked” capital allows for the compounding required for outlier success.

Consider Mercado Libre in Argentina, which delivered a 130x return over 26 years, or GloBant, which saw a 50x increase. These returns were only possible because the capital was committed for the long haul, protecting the “Learning Machine” entrepreneurs from the volatility of public sentiment.

Three Bold Predictions for 2026

The global landscape is moving faster than the traditional financial centers can process. By 2026, three trends will define the winners of the next era:

The European Renaissance: We are seeing a surge of technical CEOs turning “deep science” into global powerhouses. This isn’t happening in London; it’s happening in Milan with Bending Spoons and Poland with Eleven Labs. These founders are building global-first companies from day one.

The Stablecoin Killer App: While the U.S. treats blockchain as a speculative toy, emerging markets are using it for survival. In regions with unstable local currencies, stablecoins account for 40% of financial transfers, compared to just 4% in the U.S. Emerging markets are leading the world in rebuilding financial infrastructure.

The New Path to Liquidity: The “death of the IPO” is a myth; it is simply being replaced by secondary private markets. High-end “Crossover Funds” are now buying assets in the private markets at premiums. Founders and employees no longer need a New York ticker symbol to find life-changing liquidity.

The Roger Bannister Effect and the Multiplier Era

In 1954, Roger Bannister ran the first four-minute mile, a feat deemed physically impossible. His record lasted only 46 days. Once the mental barrier was shattered, everyone else followed; today, over 2,200 people have done it.

This is exactly what is happening in global venture. Pioneers like Mercado Libre—now a $130 billion company—and Nubank proved that you could build a giant from Argentina or Brazil. They cleared the path for a massive “Multiplier Effect.”

Success creates a cycle: Generation 1 (E-commerce and Payments) provides the capital and mentorship for Generation 2 (Fintech and EdTech), eventually leading to the Deep Tech and AI innovations of Generation 4.

“Talent, like, real, raw, entrepreneurial talent… is everywhere in the world. It is globally distributed. Success, more than ever before, can come from anywhere.”

The Future is Elsewhere

The era of Silicon Valley’s monopoly on innovation is officially over. We have moved from a localized “Access Class” to a global game where the most resilient entrepreneurs are being born in the most challenging environments.

If talent is globally distributed but success is no longer tied to a California zip code, you must ask yourself a strategic question: where is your capital oriented? If you are still looking for the next $100 billion company in the same old places, you’ve already missed the flip. The future is “Elsewhere.”